) – A Quality Stock with Strong Fundamentals](https://www.chartmill.com/images/uploads/thumbnail_article_luc_kroeze_c1f44c837d.webp)

Fastenal Co (NASDAQ:FAST) stands out as a potential candidate for quality investors, meeting key criteria in profitability, financial health, and operational efficiency. The company, a distributor of industrial and construction supplies, has demonstrated consistent performance and solid fundamentals.

Why Fastenal Fits the Quality Investing Profile

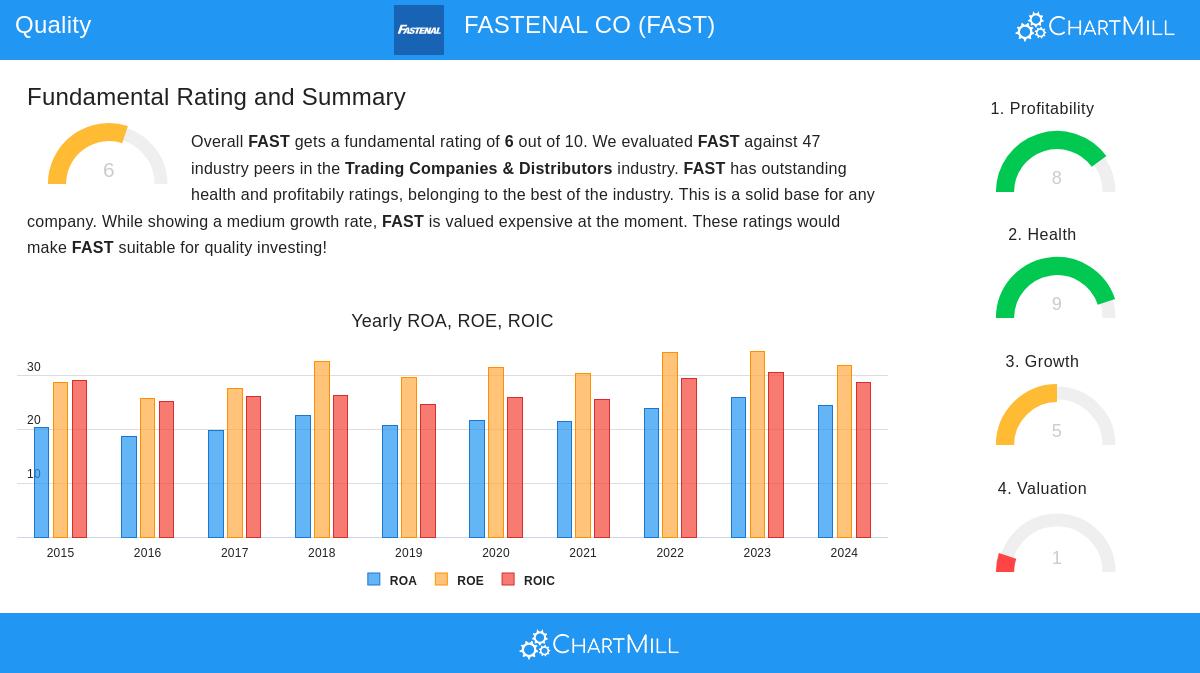

- Strong Return on Invested Capital (ROIC) – Fastenal’s ROIC of 29.89% (excluding cash and goodwill) is well above the 15% threshold for quality stocks, indicating efficient use of capital.

- Low Debt Burden – The company’s debt-to-free cash flow ratio of 0.23 suggests it could pay off all debt in less than a year, reflecting strong financial health.

- Revenue and Profit Growth – Over the past five years, Fastenal has delivered 8.33% annual revenue growth and 7.41% EBIT growth, showing steady expansion.

- High Profit Quality – With a five-year average profit quality of 87.39%, the company effectively converts net income into free cash flow.

- Profitability Metrics – Fastenal’s operating margin (19.89%) and profit margin (15.13%) rank among the best in its industry.

Valuation Considerations

While Fastenal scores well on quality metrics, its valuation appears elevated with a P/E ratio of 40.94, above both industry and S&P 500 averages. Quality investors often accept higher valuations for companies with durable competitive advantages, but further analysis is warranted.

Fundamental Analysis Summary

Fastenal’s fundamental rating of 6/10 reflects strong profitability and financial health, offset by a high valuation. Key strengths include:

- Top-tier ROIC and margins

- Minimal debt and strong liquidity

- Reliable dividend history (though payout ratio is high at 79.61%)

- Expected future revenue growth of 8.33%

For investors seeking stable, well-managed businesses, Fastenal presents a compelling case.

Our Caviar Cruise screener lists more quality stocks and is updated daily.

Disclaimer

This is not investing advice. The article highlights observations at the time of writing, but investors should conduct their own analysis before making decisions.